Overview

The following disclosures are in fulfilment of the requirements of Part 8 of the Financial Services (Investment Firms) (Prudential Requirements) Regulations 2021, which came into force on 1 July 2022.

Risk Management objectives and policies

Alvar Financial Services Limited (“the Firm”) has undertaken a comprehensive review of its Risk Management architecture, under the Enterprise Risk Management framework, this has included reviewing the Firm’s objectives and policies to ensure they align and reflect the ideals of the Firm, market best practice and regulatory compliance. This has involved a review of all aspects of the business, including the monitoring and risk controls with respect to capital requirements, concentration risk and liquidity risk, strategy, and risk profile as part of the Enterprise Risk Management framework. The purpose being to enhance the structure going forward to place the business on a stronger footing for organic growth benefiting our clients with improved services and risk management controls. The Firm has revised its Enterprise Risk Policy to ensure that this reflects the latest market best practices and regulatory expectations, this includes a concise risk appetite statement which confirms the Firm’s prudent attitude to risk. These initiatives are welcomed given that they support the Firm with a robust Risk Management control environment going forward and demonstrate management’s commitment to ensuring that the Firm is run with high standards of Risk Management and corporate governance, thus assuring investors of a well-run and established institution.

Risk appetite statement

The Firm will not accept risks that are determined as ’High’ post mitigation and controls. Further controls would need to be implemented, or the business or process is not undertaken as it would fall out of the Firm’s Risk Appetite.

In addition, the Firm has a zero tolerance towards financial crime, including but not limited to: money laundering, fraud, market abuse, terrorist financing, bribery, and corruption.

Risks are evaluated in the Risk Register using the following methodologies:

- Quantitatively: Expected impact primarily on capital (annualised profit/loss impact) or liquidity

- Qualitatively: Level of reputational or operational impact (where impact to capital and liquidity is difficult to quantify and/or less applicable)

Level 1 risk categories identified across the group are as follows: Business Risk, Financial Risk, IT Risk, Legal, Compliance & Financial Crime Risk and Operational Risk. We have identified the following as focal areas for 2025: Business Continuity, Concentration Risk, Compliance Risk, and Trading Risk.

The Firm's Enterprise-wide risk framework encompasses mitigant controls against each identified risk. Controls are assessed against effectiveness and any shortfalls are either strengthen, substituted and/or remediated accordingly.

The Firm upholds a strong culture which promotes ethical behaviour, accountability, and informed decision-making at all levels. It ensures that employees understand, own, and manage risks proactively, aligning with the organisation’s strategic goals and regulatory expectations.

Governance

As with Risk Management the Firm has reviewed its Corporate Governance arrangements. This has included a review of the structure of board committees, their terms of reference, management meetings and their terms of reference. The purpose being to align the various components of Corporate Governance to ensure that committee and management meetings, terms of reference reflect a proper oversight of the Firm and its activities to ensure that these align with policies and procedures, regulatory obligations and market best practice.

The Firm has a dedicated Risk Management forum which reports to a Board Committee on a quarterly basis and a Management Meeting on a monthly basis. This allows for the function to be able to expose to the Board and management body any matters of concern which need to be reported and addressed.

The number of directorships held by each member of the Board and management body in Gibraltar at 31 December 2025 was as follows:

- A T McGrath (3)

- M C Leadbeater (2)

- J M Wilson (2)

- J C Page (2)

The composition of the Board and management body reflects the Firm’s adherence to diversity. The Firm encourages diversity and recruits members to the Firm at all levels on the basis of their skills and experience and not their gender, ethnic background or any other consideration. The primary motivator being what the team member brings to the Firm to enhance the operational architecture and effectiveness of the Corporate Governance infrastructure.

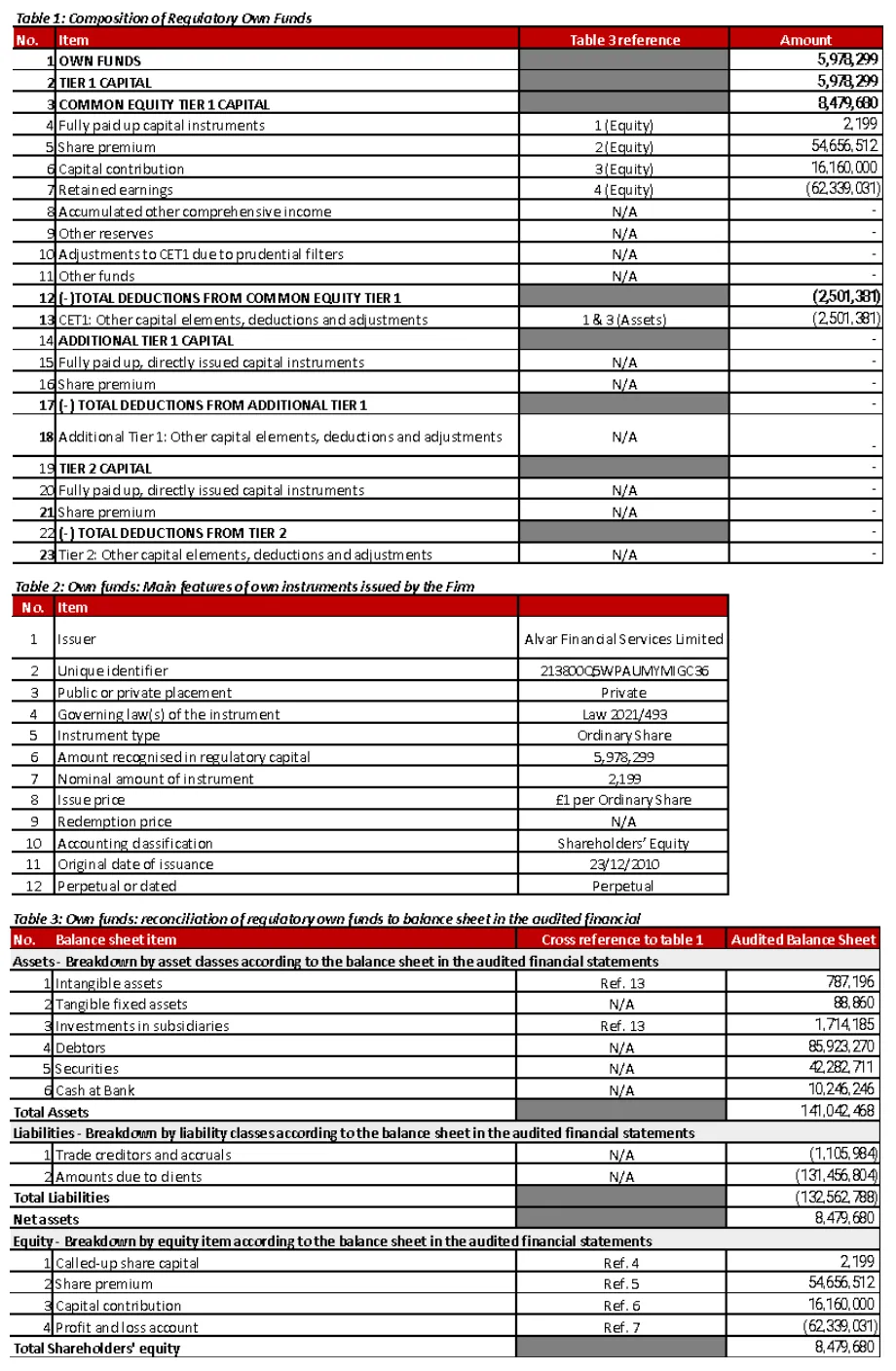

Own Funds

The Firm continues to meet the Own Funds as set out in the regulatory standards. All the necessary deductions have been applied in determining Own Funds.

In determining the Firm’s Own Funds, intangible assets and investments in subsidiaries have been deducted in full. The Firm’s Own Funds at 31 December 2025 were £6.0 million after deducting intangible assets (£0.8 million) and investments in subsidiaries (£1.7 million) from its audited Net Assets (£8.5 million).

The Firm’s Own Funds is made up entirely of Common Equity Tier 1 capital. The Firm does not have any Additional Tier 1 or Tier 2 Capital. The Firm’s Common Equity Tier 1 capital is made up of fully paid-up shares.

No restrictions have been applied to the calculation of Own Funds.

The following tables present the Firm’s own funds composition, the main features of its capital instruments, and a reconciliation of own funds to the audited balance sheet as at 31 December 2025. All amounts are in GBP.

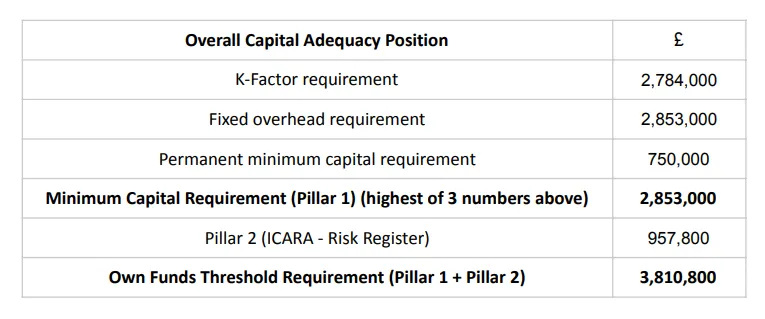

Own Funds Requirements

The Firm’s prudential classification is as a Class 2 Investment Firm.

The Firm’s Own Funds requirements have been comfortably met, and the Firm continues to improve its financial performance. Management will continue to recommend to the Board that any surplus funds generated will continue to be added to reserves for the foreseeable future in order to continue to strengthen the Firm’s Own Funds. At all times the Firm has performed within its Own Funds requirements.

The Firm’s approach to assessing the adequacy of its internal capital to support current and future activities is undertaken through a budget based on appropriate estimates of costs to sustain the business and grow against expectations. This is also done through the ICARA process, where Risk Management plays an integral role in allocating capital against future risks. The Board reviews the Firm’s capital surpluses and actual results against budget quarterly.

The Firm Own Funds Requirements have been determined by following the Investment Firms Prudential Regime (“IFPR”) three-pillar approach:

Pillar 1 – Minimum capital requirement

The minimum capital requirement is the higher of the ‘permanent minimum capital requirement’, ‘fixed overhead requirement’, and ‘K-Factor requirement’.

The permanent minimum capital requirement acts as a floor for all levels of capital required under the IFPR and must be at least the initial capital requirement. Alvar’s initial capital requirement is £750,000.

The Fixed Overheads Requirement (“FOR”) should be at least one quarter of the fixed overheads of the preceding year (i.e. 2025). The Company’s FOR has been calculated as being at £2,853,000.

The IFPR uses quantitative indicators (“K-factors”) to specifically target those services and business practices that are most likely to generate risks for a particular investment firm. K-factors are divided into three groups, and they aim to capture the risk an investment firm can pose to clients (Risk-to-Client (“RtC”)), to market access (Risk-to-Market (“RtM”)) and to itself (Risk-to-Firm (“RtF”)).

At 31 December 2025, the Firm’s aggregate K-factor requirement was £2,784,000, made up an RtC of £656,000, an RtF £2,044,000 and an RtM of £84,000.

Pillar 2 – ICARA

The Firm maintains a comprehensive Risk Register of all risks it may face.

Each risk has undergone an inherent risk assessment (considering probability of occurrence and financial impact) to determine its Inherent Risk Score and is then assigned controls from the Firm’s Control Risk Framework to determine its Residual Risk Score and, finally, the Residual Financial Cost (i.e. its Pillar 2 capital requirement).

The Risk Register generates a Pillar 2 capital requirement of £957,800 across all risk areas.

Remuneration policy and practices

The Firm’s pay strategy is designed to reward competitively the achievement of long-term sustainable performance and attract and motivate the very best people, regardless of gender, ethnicity, age, disability or any other factor unrelated to performance or experience, while performing their role in the long-term interests of our stakeholders.

To achieve this objective, the Firm believes that effective governance of its remuneration practices is a key requirement. The design and implementation of remuneration policies are overseen by the Remuneration Committee to ensure what the Firm pays its people is aligned to the Firm’s business performance and strategy. Performance is judged not only on what is achieved over the period but more importantly on how it is achieved, as the Firm believes the latter contributes to the long-term sustainability of the business. Total compensation (fixed pay and variable pay) is the key focus of the Firm’s remuneration framework, with variable pay (primarily bonus pools and annual incentives) differentiated by performance, conduct and adherence to the Firm’s values.

The remuneration arrangements of the Firm have been designed in a manner that:

(i) is consistent with and promote sound and effective risk management;

(ii) does not encourage risk-taking that is inconsistent with the risk profile of the Firm; and

(iii) does not impair compliance with the Firm’s duty to act in the best interests of the clients

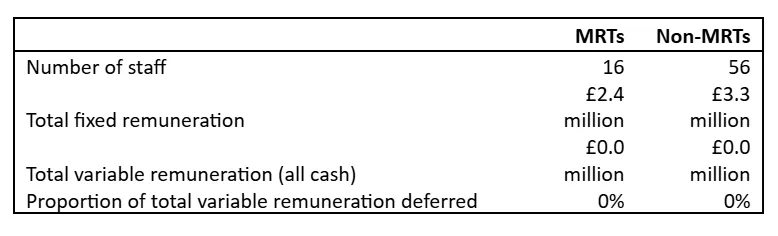

All remuneration paid to staff in 2025 was in cash (other than contributions to workplace pensions and benefits such as health insurance and life assurance). The Firm does not award any deferred remuneration.

Remuneration for 2025 is broken down as follows and is split between material risk takers (“MRTs”) and non-MRTs:

No severance payments were awarded in 2025 that related to 2024. Severance payments totalling £26,205 were awarded to 18 individuals in 2025, all of which was paid in 2025. The highest payment awarded to a single individual was £12,942.

Neither Regulation 85(6) nor 85(7) apply to the Firm.

Investment Policy

The Firm doesn’t meet the criteria as provided by Regulation 85(6) and as such it is exempted from the Investment Policy disclosures.

Environmental, social and governance risks

The Firm doesn’t meet the criteria as provided by Regulation 85(6) and as such it is exempted from the Environmental, Social and Governance Risks disclosures.